Whether it’s a boozy trip home after a long night out or just another trip to your regular pig-out spot a mere 15 minutes away, I’m sure we’ve all been tempted by the convenience of Uber and Grab.

This is perfectly understandable, given that promotional codes can bring the estimated fare of an Uber ride close to or even lower than a typical adult bus fare.

Or do they really?

Falling Victim To Hidden Charges

It was only recently when I checked my account transactions that I found out I’d been overcharged for one of my trips, effectively voiding the promotional code I happily punched in at the start of that week.

Upon this sudden realization, it made me question the integrity of the application and the hidden charges incurred for my past trips.

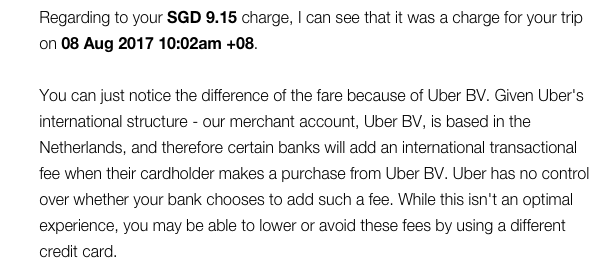

So I e-mailed Uber (thankfully they’re pretty responsive with their customer service) regarding the actual deducted fare, that amounted to $12+ instead of the $9.15 that was initially displayed on my application when I booked the ride.

This was the reply I got from their customer service representative:

TL;DR: What they’re basically saying is that due to exchange rates and their merchant account being based in Netherlands, certain banks DO charge a transactional fee, resulting in that few dollars difference.

While I’m not entirely sure if the trips I took prior were affected, this was definitely an eye-opener on how meticulous we should be with online transactions and terms and conditions, even with an established brand like Uber.

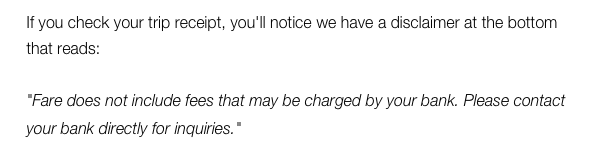

To be fair, they do put the disclaimer at the bottom of every receipt. But what’s the point of putting the disclaimer at the end of a receipt when the payment has already been made?

The receipt’s function, in this case, is to reflect the specified amount of cash given in exchange for the service. The inaccuracy of the receipt is a concerning issue.

Apparently, Being Overcharged With Extra Fees Is Normal

A post by The Straits Times early last year affirmed the issue of overcharging and the worrying lack of transparency from the company.

“The Uber receipt shows one figure and the credit-card statement, another,” says 43-year-old business development director Wei Chan, who uses Uber roughly 10 times a month.

In this e-payment culture that we live in now, it is no surprise that many of Uber’s users have debit or credit as their main payment method.

According to an interview with The Straits Times, local banks and foreign banks do not impose these extra fees and instead, relevant credit or debit card schemes are the ones responsible for the additional costs.

Again, the issue of transparency resurfaces as Uber mentioned the extra charges source from the respective banks but as clarified by local and foreign banks, they are not the ones imposing the extra charges.

What You Can Do

Since the reporting of overcharges early last year, Uber has introduced multiple ways of paying, including cash payment which seems like the most upfront way of paying for services without the baggage of back end processes e-payments usually come with.

Since the reporting of overcharges early last year, Uber has introduced multiple ways of paying, including cash payment which seems like the most upfront way of paying for services without the baggage of back end processes e-payments usually come with.

They did provide me with alternatives to avoid similar complications, which is to either pay by cash (I guess cash is indeed king after all) or use a different card to charge.

Do check with your respective banks on how they charge and take note of your transaction history because you could end up like me – losing out on dollars equivalent to a plate of chicken rice on an already rainy day.

{kind=link}