")

Can a fresh graduate starting their career afford a condo / apartment? If you are an undergraduate or fresh graduate thinking of buying a private home, then you have come to the right place.

In this article, we look at what fresh graduates can afford in the private home sector across all the districts in Singapore (excluding landed homes).

What This Means

What This Means

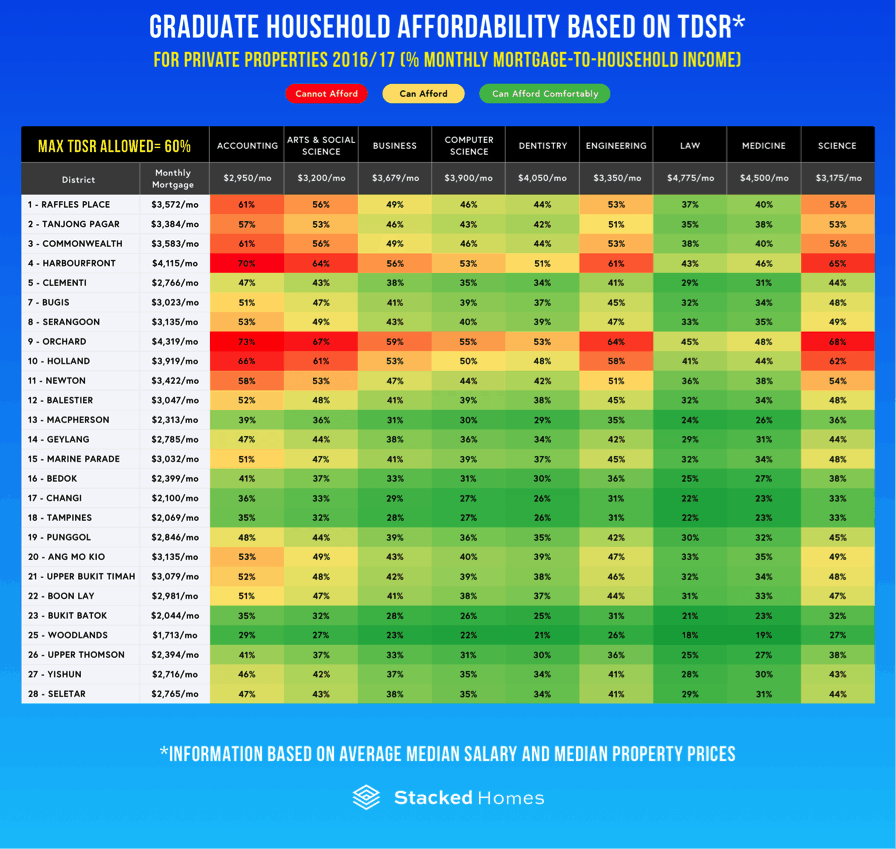

The median graduate salary for each faculty can be seen on the 2nd row. The median monthly mortgage payment required for each district is listed in the 2nd column.

To simplify things, we derived the TDSR by assuming a household income of 2 graduates from the same faculty and together, they form a household.

Median prices are obtained from URA and we only consider homes that are 100 Sqm / 1076 Sqft or less to remove large homes that graduates are unlikely to purchase, and the prices of which may skew our data.

To determine if they can purchase the home, we assume that they can pay the necessary upfront costs (e.g. taxes and the 20% down payment).

With that out of the way, their affordability is determined by whether they can fulfil the Total Debt Servicing Ratio (TDSR). As of October 2017, the TDSR stands at 60%. We assume that the household has no other debt (e.g. personal loan, car loans, credit cards etc.)

Finally, we only cover graduates from the following faculties: Accounting, Arts & Social Science, Business, Computer Science, Dentistry, Engineering, Law, Medicine and Science.

Graduate income data is obtained from NUS.

The resulting figures show the monthly mortgage payments as a percentage of household income. Anything above 60% has breached the TDSR limits and is not allowed.

It’s Green For Us, So We Can Afford It!

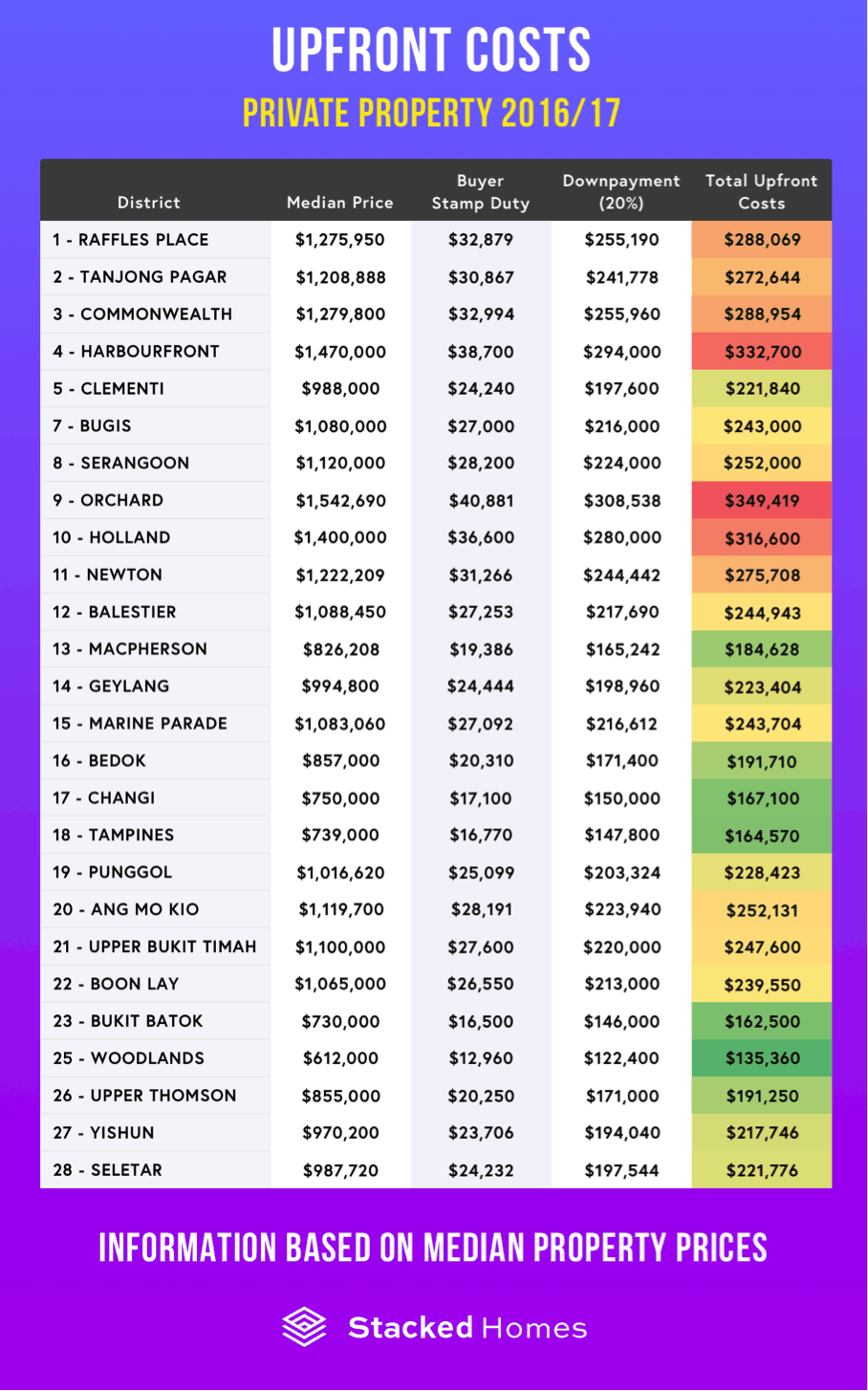

Now before you think about splashing around the condominium pool on the weekends, take note that the table above only shows whether you qualify under the TDSR rule. Qualifying does not equate to having the ability to purchase a private home – the upfront costs for private homes are off the charts to a fresh graduate!

Apart from having little to no savings (like most fresh graduates) and an overhanging student loan, owning a condominium incurs other costs like legal fees, maintenance and higher taxes.

This reduces your cash flow early on in life that can potentially be used to invest for higher returns, or saved up to start a business someday.

Here’s the cash you need upfront to buy a condominium / apartment:

So, most graduates can technically afford a loan, but unless you strike the lottery or have parental blessings, it could take a long time to save up for that down payment.

This article is provided by Stacked Homes, where you can buy, sell or rent HDB and Condos directly in Singapore.

{kind=link}